Recently, the results of listed companies on the Shanghai and Shenzhen stock exchanges for the full year of 2021 and the first quarter of 2022 have been disclosed. According to the announcement of listed companies, after statistics of the performance of 52 cathode materials and upstream raw materials listed companies, it is found that the performance of industry chain companies in the first quarter of 2022 will continue to improve.

Although there are as many as 47 companies that have achieved growth in both operating income and net profit in 2021, and only 39 in the first quarter of 2022, from the perspective of total net profit, in the first quarter of this year, the 52 listed companies included in the statistics, the profit in just one quarter is close to half of the full year profit in 2021. The following are details on the summary of the cathode materials companies performance, for more information, please read this article.

1.Revenue and net profit go hand in hand

From the perspective of operating income, the 52 listed companies of cathode materials and upstream raw materials included in the statistics will have a total operating income of 938.469 billion RMB in 2021, with an average operating income of 18.047 billion RMB. Among them, except for the slight decrease in operating receipt of PENGXIN, the remaining 51 companies have achieved positive growth. Specifically, 15 companies, including ZIJIN, CMOC, SRBC, sinochem, CHENGTUN, WESTERN, HUAYOU, Shanshan, CNGR, GEM, XTC, Salt Lake, Ganfeng, BTR and RONBAY, , have achieved operating revenue of more than 10 billion RMB. Among them, the operating income of ZIJIN and CMOC exceeds 100 billion RMB. More companies have doubled their operation revenue, reaching 18, namely Shanshan, CNGR, Ganfeng, BTR, RONBAY, EASPRING, TIANQI, CHANGRMB LICO, ZEC, TENGRMB, Lopal, KANHOO, FANGRMB, Youngy, FENGRMB, Zhongyin, XINGYE, and Dynanonic and this number up from just one in 2020.

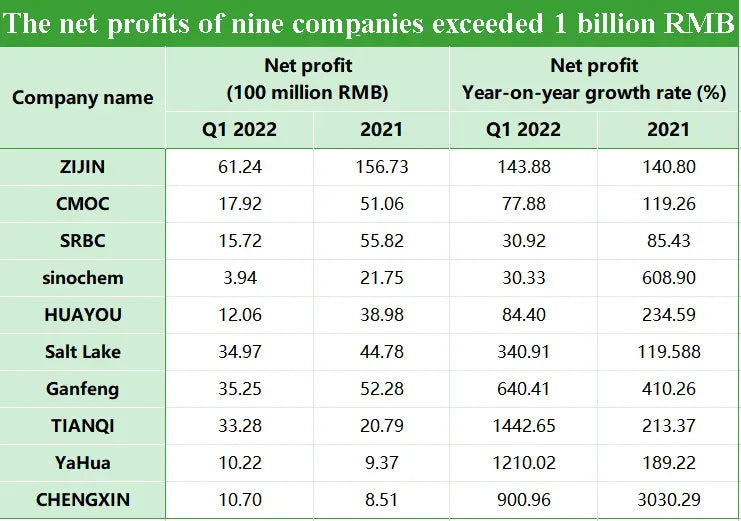

In the first quarter of 2022, 52 companies totaled 270.2 billion RMB, with an average operating revenue of 5.196 billion RMB; Among them, ZIJIN, CMOC, sinochem, SRBC and HUAYOU exceeded 10 billion RMB in revenue. Operating revenue of 20 companies more than doubled year-on-year, but there were also seven companies with negative revenue growth. In terms of net profit, the total net profit of the 52 listed companies included in the statistics is 69.535 billion RMB in 2021, with an average net profit of 1.337 billion RMB. Among them, ZIJIN, SRBC, CMOC, sinochem, CHENGTUN, WESTERN, HUAYOU, Shanshan, Salt Lake, Ganfeng, BTR, Easpring, TIANQI, TENGRMB and other 14 companies have net profits of more than 1 billion RMB. Although there are four companies with negative net profit growth, but no loss, all profit.

In the first quarter of 2022, the net profits of 52 listed companies totaled 33.172 billion RMB, with an average net profit of 638 million RMB. Among them, ZIJIN, CMOC, SRBC, HUAYOU, Salt Lake, Ganfeng, TIANQI, YaHua and CHENGXIN have net profits of more than 100 million RMB. 28 companies doubled their growth, among which, share of Youngy, increased by nearly 140 times, TIANQI, YaHua, CJN and Dynanonic increased by more than 11 times; Nine companies showed negative growth, while only three saw a loss of up to 14 million won.

It is worth noting that among the 52 listed companies, 7 companies in the first quarter of 2022 have more net profit than the whole year of 2021, respectively TIANQI, YaHua, KANHOO, Jiangte , CHENGXIN, SINOMINE, Youngy. Another 14 companies, including Salt Lake, Ganfeng, ZEC, SICHUAN NEW ENERGY POWER, Lopal, TIANQI, FULIN P.M., SPLENDOR, Hezong, XIANGTAN ELECTROCHEMICAL, FENGRMB, Tibet Mining, PENGXIN, Dynanonic, have exceeded half of the annual net profit of last year.

In general, since 2021, the performance of cathode material and upstream raw material listed companies has maintained a fairly high level. Last year, 52 companies were profitable, and the overall net profit in the first quarter of this year was even more extraordinary, which was nearly half of the whole year of last year. The main reason is that since the end of 2020, the prosperity of the battery industry has picked up, the volume and price of battery materials and upstream raw materials have risen together, leading companies are basically full production and full sales, greatly boosting the performance of industrial chain companies.

2.Market and demand win-win

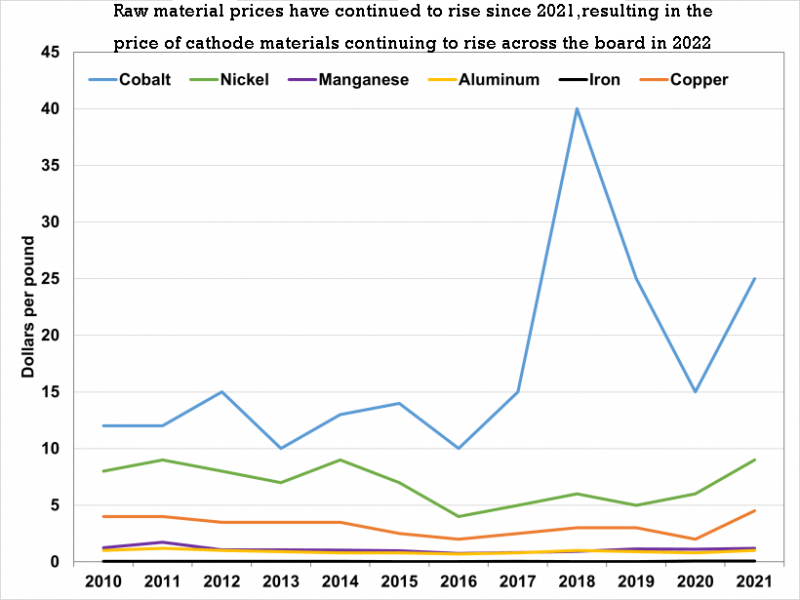

From the point of view of market price, since 2022, the price of cathode materials continues to rise in the situation of raw materials lithium, cobalt and manganese. Data show that raw material prices have soared since 2021. As of April 27, 2022, compared with January 1, 2021 (the same below), the price of nickel, cobalt, electrolytic manganese, lithium carbonate and lithium hydroxide have increased by 84%, 99%, 20%, 798% and 818% respectively. Driven by the price of raw materials, the price of cathode materials has also risen sharply, ternary 523 material up 195%, ternary 622 material up 177%, ternary 811 material up 149%, lithium iron phosphate material up 341%.

It is worth noting that on April 27, the price of lithium concentrate again set a record high price. In the first auction of lithium concentrate in 2022 held by Australian lithium miner Pilbara, the auction volume of ore was 5000 tons, and the concentrate taste was 5.5%, and the auction price was $5650 / ton. Far more than the current lithium concentrate about $3,100 / ton mainstream price.

In terms of cathode material output, data released by the Lithium Branch of China Non-ferrous Metals Industry Association showed that China's cathode material output in 2021 was about 1,111,700 tons, an increase of about 100.78% year-on-year. Among them, 101,000 tons of lithium cobalt, 440,500 tons of ternary materials, 459,100 tons of lithium iron phosphate and 11,100 tons of lithium manganese were produced.

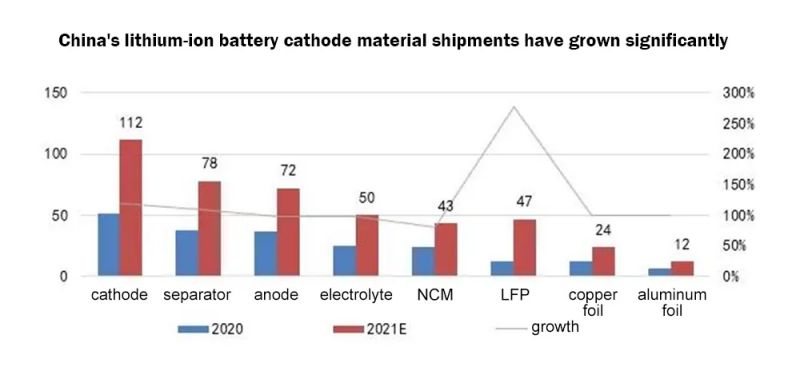

In terms of cathode material shipments, data from The White Paper on The Development of China's Lithium-ion Battery Cathode Material Industry (2022) show that the shipments of cathode materials in China in 2021 were 1.094 million tons, with a significant year-on-year increase of 98.5%. Among them, shipments of lithium iron phosphate cathode materials reached 455,000 tons, and ternary cathode materials reached 422,000 tons. In 2021, the output value of China's cathode materials reached 141.91 billion RMB, up 123.1 percent year on year, exceeding the growth of output value in 2017.

From the perspective of cathode material investment and production expansion, relevant institutions made statistics on the investment and production projects of battery new energy industry chain in 2021 according to the announcements and public reports of listed companies. Among them, 317 projects and 281 announced investment amounts were counted, with a total investment of more than 1.27 trillion RMB. Among them, in the field of cathode materials and upstream raw materials, 76 of the 91 projects included in the statistics announced the amount of investment, with a total investment of about 285.302 billion RMB.

In 2022, cathode material manufacturers continue to increase production capacity, and listed companies frequently enter the market: Dynanonic plans to invest 7.5 billion RMB to build a new phosphate cathode material production base; YONFER plans to invest 3 billion RMB to build iron phosphate and lithium iron phosphate production line; WANRUN science and technology innovation board IPO was accepted, proposed to raise 1.262 billion plus lithium iron phosphate; Together with YONFER, GEM has expanded the production of 150,000 tons of iron phosphate and 100,000 tons of lithium iron phosphate materials within 2 years. FENGRMB plans to raise capital to expand production of 50,000 tons of lithium iron phosphate cathode materials, and plans to invest 1 billion RMB in Yuxi city to build 200,000 tons of lithium battery high-energy cathode materials and related projects......

3.Summary

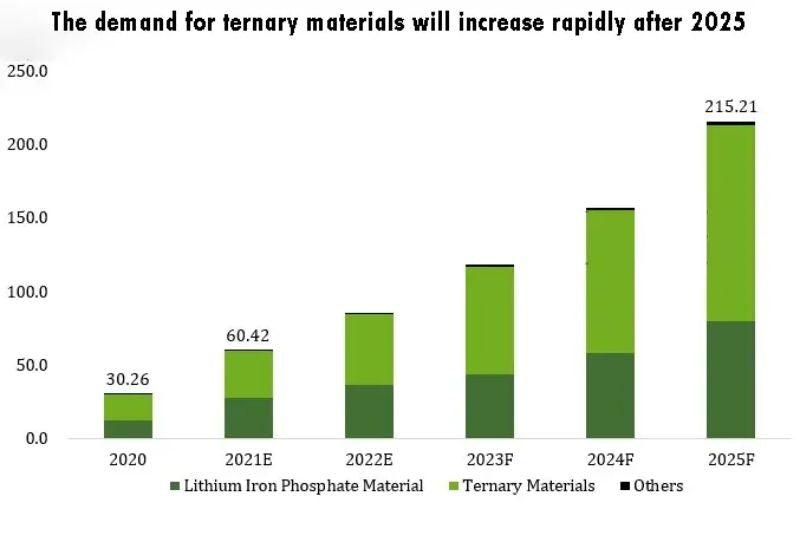

Looking forward to the future, one in the industry analysis, as the global new energy automobile permeability continued ascension and the carbon targets gradually, the demand of automobile power battery and energy storage battery will last with high speed growth, and 2030 years ago, other battery system is still difficult to large-scale industrialization, lithium ion battery will still be the mainstream. The industry expert predicted that global shipments of lithium-ion batteries would grow at a compound growth rate of 25.6 percent until 2030, with total shipments approaching 5TWh by 2030. Another expert predicted that the upstream lithium carbonate segment would be in a tight balance in the next five years; In the field of cathode materials, the capacity of lithium iron phosphate materials is too tight before 2025, and the demand for ternary materials will rise rapidly after 2025.

In the market demand, cathode material industry chain related enterprises will continue to benefit. From the competitive landscape, an industry insider pointed out in the white paper that the cathode material industry compared to other industries, the overall market concentration is low, the top ten enterprises combined market share is less than 50%. In the future, as battery enterprises, chemical enterprises and upstream mineral enterprises cross into the field of cathode materials, the competition in the whole industry may become more intense, and the overall industry pattern is still likely to change greatly. At a time when the need for high-energy-density lithium-ion batteries is urgent, as the key to improve the energy density of lithium ion batteries, the high voltage cathode materials for lithium ion batteries have great development prospects, which may bring new development ideas for cathode material enterprises