Main content:

- China's energy storage power shipments are expected to exceed 90GWh in 2022, and power storage will remain No.1

- Lithium battery prices will continue to be high, and Q4 will gradually loosen in 2022

- Long-term energy storage in China will be more popular with policy and capital support

- The reform of electricity marketization is expected to accelerate, and the energy storage business model will become more mature

- The outbreak of global demand continues to drive China's leading companies to accelerate their global layout

- More central and state-owned enterprises will join the energy storage track in China

On April 21, 2021, two ministries and commissions of the Central Government issued the Guidance on Accelerating the Development of New energy storage (Draft), requiring the installed capacity of new energy storage to reach over 30 million kw by 2025. In February 2022, the two ministries and commissions officially issued the implementation Plan for the Development of New Energy Storage during the 14th Five-year Plan period, requiring that by 2030, the core technology and equipment of new energy storage should be independent and controllable, technological innovation and industrial level should be at the forefront of the world, and the development should be deeply integrated with all aspects of the power system to fully support the realization of the carbon peaking target in the energy sector as scheduled. As an important parameter in new energy storage technology, the new method for battery capacity estimation is also an important part of technological innovation. Here's the view on the development trend of the energy storage market in 2022, there are six trends in China's energy storage industry in 2022.

1.China's energy storage power shipments are expected to exceed 90GWh in 2022, and power storage will remain No.1

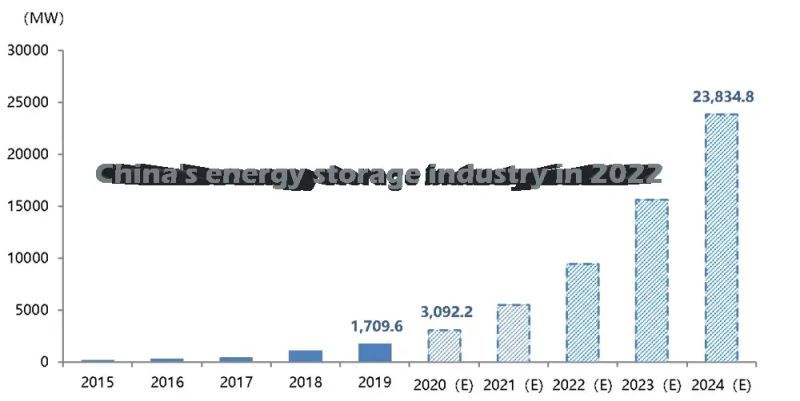

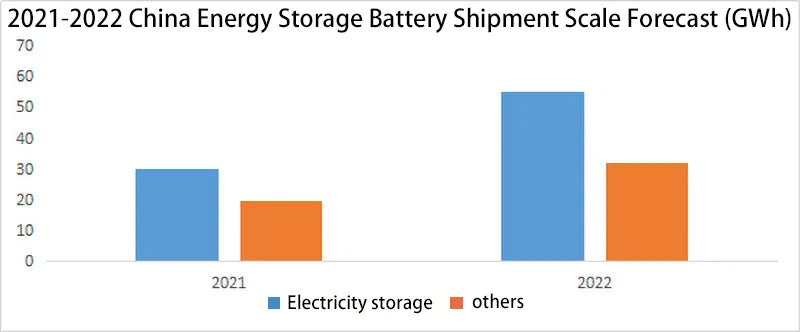

According to detailed statistics, domestic energy storage battery shipments in 2021 will be 48GWh, a year-on-year increase of 2.6 times; of which power energy storage battery shipments will be 29GWh, a year-on-year increase of 4.39 times compared to 6.6GWh in 2020. The reason behind the growth is due to the surge in the installed capacity of overseas energy storage power stations in 2021 and the management policy of domestic wind and solar energy storage. GGII predicts that domestic energy storage batteries are expected to continue to maintain a rapid growth trend in 2022. It is conservatively estimated that annual shipments are expected to exceed 90GWh, an increase of 88% year-on-year.

Affected by factors such as the domestic dual carbon target and the high level of overseas energy inflation, the power generation side, grid side and large industrial and commercial user side will remain the largest downstream application of energy storage. In particular, due to the strict implementation of carbon emission reduction in overseas Europe and the encouragement of subsidy policies for energy storage purchases in the United States and Australia, energy storage equipment will still be in short supply in the next 1-2 years. Electric energy storage is expected to ship close to 60GWh in 2022.

In addition, segmented application scenarios such as communications backup power, global home storage exports, and portables will also maintain rapid growth. It is expected that the shipments of other segments such as communication backup power, home storage and portable are expected to reach 30GWh in 2022. Taking the global home storage as an example, the electricity price of residents in developed countries around the world is 2-3 times that of China.

The high electricity price has always been the fundamental driving force for the outbreak of global home storage demand, which has also directly led to the current situation of home storage products in short supply. Home storage giant Tesla mentioned in its Q2 earnings conference call in 2021 that the production capacity of its Megapack energy storage products has been sold out by the end of 2022. In 2022, due to external tensions and high levels of energy inflation in Europe and the United States, China's exports of home storage shipments are expected to double on the basis of 2021.

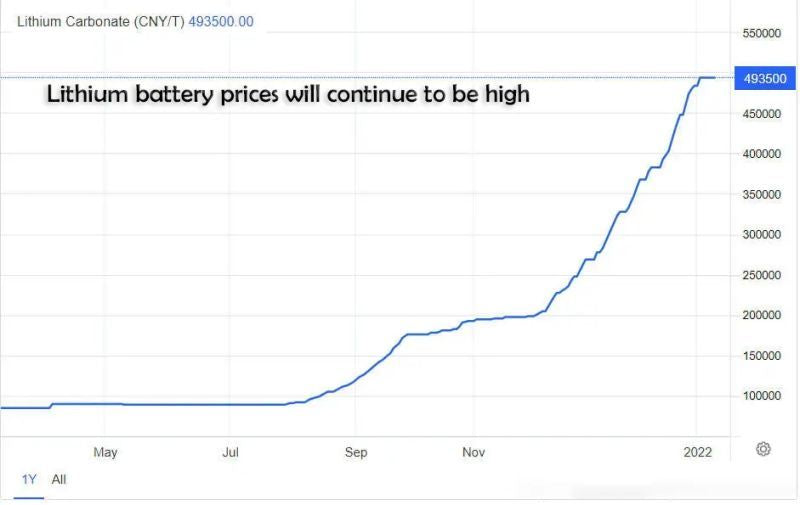

2.Lithium battery prices will continue to be high, and Q4 will gradually loosen in 2022

In 2021, the shortage of the four major upstream materials and the rapid expansion of downstream demand will lead to an increase in the cost of lithium batteries instead of decreasing. As of February 2022, the cost of lithium batteries is still high and volatile. On the lithium salt side, it is predicted that the price of lithium salt is expected to remain at a high level of more than 300,000 yuan per ton in 2022. The demand for lithium salt throughout the year is still greater than the supply of lithium ore, and the market supply and demand is still in a state of tension. In 2022, the new increase of global lithium salt is limited. Considering the disturbance of political and even religious factors such as the attempts to nationalize lithium mines in Mexico and Chile, the expansion and import of lithium mines will not be smooth sailing, and the high cost of lithium salts will be a high probability event.

On the cathode material side, cathode material companies themselves have low bargaining power, and their price fluctuations are mainly determined by upstream lithium salts. At present, the processing fee in the field of cathode materials is gradually decreasing, but the increase in the price of upstream raw materials has led to an increase in the cost of cathode materials, resulting in an increase in their corresponding costs. The increase in the price of cathode materials for energy storage lithium batteries (mainly LFP) is mainly driven by the increase in the prices of lithium salts and iron phosphate. At the same time, with the increase in the prices of phosphoric acid and monoammonium phosphate, the cost of iron phosphate materials continues to rise, and lithium iron phosphate materials continue to rise. Prices will remain high until Q3 2022.

On the electrolyte side, the price of H1 products in 2022 is still at a high level due to the skyrocketing prices of main raw materials. With the continuous release of new production capacity of lithium hexafluorophosphate and VC and other materials, the tension in the supply chain of the upstream electrolyte industry is expected to gradually ease after Q1 in 2022. On the anode material side, since Q4 2021, affected by the dual control policy and the increase in graphite processing prices, the price of lithium battery anode materials has risen by more than 10%. In 2022, the anode production capacity will be sufficient, especially after the end of the Winter Olympics, the graphitization production and power restrictions will be relaxed, the capacity utilization rate will increase, and the supply and demand relationship will be eased after 2022 Q3. At the same time, a new round of needle coke and graphitization will be put into production in the future, which will boost the cost and price of anodes in the long run.

On the copper foil side, the strong downstream demand in 2021 will drive the limited release of superimposed copper foil production capacity, and the price of lithium battery copper foil will continue to rise. Since the expansion cycle of diaphragms is about 1.5-2.5 years, the growth rate of the new energy market in 2021 will exceed expectations to stimulate large-scale expansion of diaphragm enterprises. In 2022, the new capacity of lithium battery copper foil will be small, the supply and demand of the industry will remain tight, and the price is still expected to maintain a slight upward trend. To sum up, it is expected that in 2022, the price of lithium energy storage batteries (LFP) in China will usher in a new round of increases, with an annual increase of between 15% and 30%. After 2023, with the gradual release of upstream raw material production capacity, the current situation of high raw material prices will be alleviated, driving the cost of power batteries to decline. Affected by this, some energy storage projects are expected to delay investment and construction until the second half of this year to buffer the financial pressure caused by rising costs.

3.Long-term energy storage in China will be more popular with policy and capital support

According to the length of energy storage, the application scenarios of energy storage can be divided into short-term energy storage (<1 hour), medium and long-term energy storage (1-4 hours) and long-term energy storage (≥4 hours, some foreign countries define ≥8 hours) Three categories. Long-term energy storage power stations are just-in-demand new infrastructure projects with a high proportion of renewable energy being connected to the grid on a large scale. Throughout the world, developed regions such as the United States, the United Kingdom and the European Union have invested a lot of money to promote long-term energy storage project demonstrations and technology upgrades.

For example, the "Energy Storage Challenge Roadmap" issued by the US Department of Energy specifies the application scenarios, cost reduction goals and cost reduction paths of long-term energy storage such as pumped storage, compressed air, all-vanadium liquid flow, and hydrogen energy storage. The UK Department of Business, Energy and Industrial Strategy plans to allocate 68 million pounds to support long-term energy storage demonstration projects in the country, covering compressed air, hydrogen energy storage, heat storage, flow batteries, metal-air batteries and other promising long-term energy storage technologies .

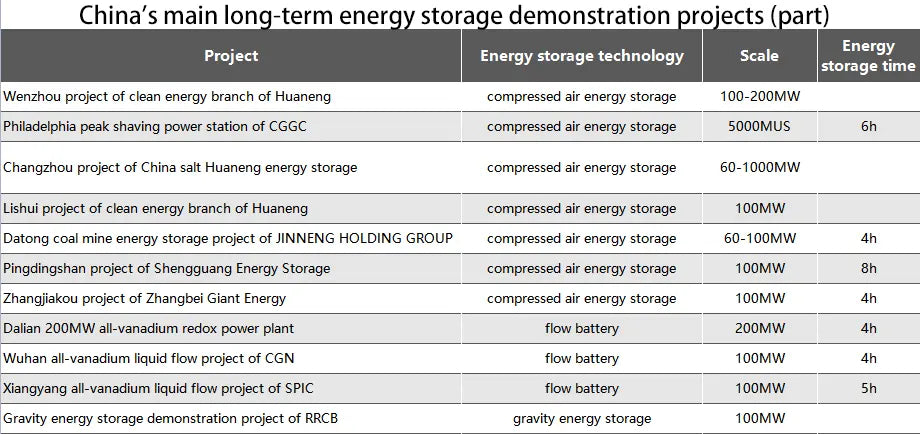

Since 2022, China is making efforts in policy, industrial support and project demonstration, and long-term energy storage products have shown a vigorous upward momentum. On the policy side, the "14th Five-Year Plan for New Energy Storage Development Implementation Plan" mentions "promoting the construction of new energy storage projects such as long-term electric energy storage, hydrogen energy storage, and thermal (cold) energy storage", and the demonstration work focuses on " Application of 100 MW advanced compressed air energy storage system", "Industrial application of vanadium flow battery, iron-chromium flow battery, zinc-Australia flow battery, etc.", "Hydrogen storage (ammonia) from renewable energy, hydrogen-electric coupling, etc. Demonstration application of recovery energy storage”.

On the project side, China's compressed air energy storage and flow battery energy storage have entered the 100 MW demonstration stage, such as China's first 100MW/400MWh Zhangjiakou advanced compressed air energy storage demonstration project, which was officially connected to the grid in January 2022; The world's largest 100MW all-vanadium redox flow battery energy storage and peak shaving power station in Dalian entered the single module commissioning stage.

It is expected that in 2022, there will be more long-term energy storage demonstration projects such as 100-megawatt compressed air and flow batteries planned or signed. As the scale of the industry continues to grow, it is expected that in 2022, a number of long-term energy storage seed companies will emerge in China, which will become the focus of local policies and capital support and care.

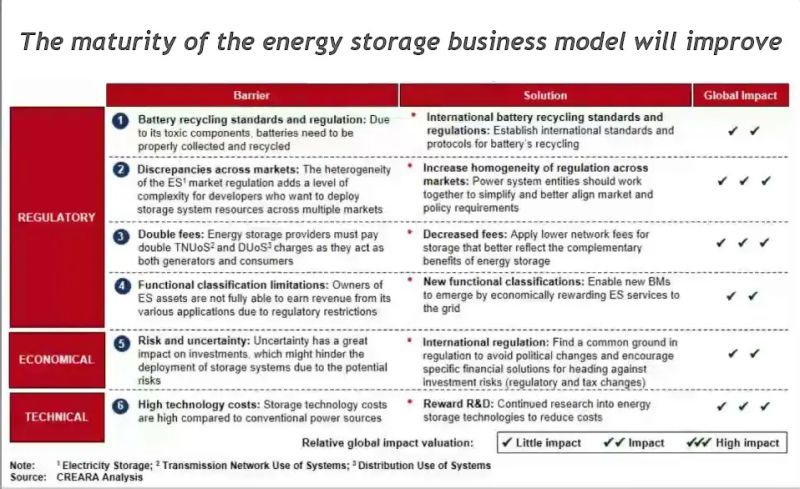

4.The reform of electricity marketization is expected to accelerate, and the energy storage business model will become more mature

Since 2022, China's ministries and commissions have issued key policies on the power market and energy storage, including regulations on The Management of Power Grid Connection operation, Administrative Measures on Auxiliary Power Services and Implementation Plan for the Development of New Energy Storage during the 14th Five-year Plan period, repeatedly clarifying the development direction of market-oriented energy storage operation.

Among them, the "Administrative Measures for Electric Power Auxiliary Services" mentioned that "on the basis of market-oriented transactions of peak shaving auxiliary services at this stage, continue to promote frequency regulation, backup, moment of inertia, climbing and other varieties to determine auxiliary service providers through market competition. , form transaction prices, reduce the cost of system auxiliary services, and better play the decisive role of the market in resource allocation.

The "14th Five-Year Plan" New Energy Storage Development Implementation Plan" Market, auxiliary service market and other construction progress, and promote energy storage as an independent subject to participate in various power markets.” The above statements on the electricity market and energy storage’s participation in market transactions are in the same line, but at the same time go a step further. The promotion and popularization of the electricity spot market will help The commercial operation of energy storage has given a boost.

In this context, it is predicted that the pilot promotion of the electricity spot market will accelerate in 2022, and more places will issue supporting policies and implementation rules for energy storage to participate in the regional electricity capacity market, ancillary service market and spot market. By the end of 2022, there will be more demonstration provinces to form a market-oriented principle of "whoever provides, whoever benefits; whoever benefits, who bears", build a power cost transmission mechanism that can run through to the user side and can cover the low-carbon and clean exterior. The overall social cost dredging system will be adopted. At that time, the enthusiasm for investment in energy storage assets will be insufficient, and the problem of focusing on construction and ignoring operation will be alleviated to a certain extent.

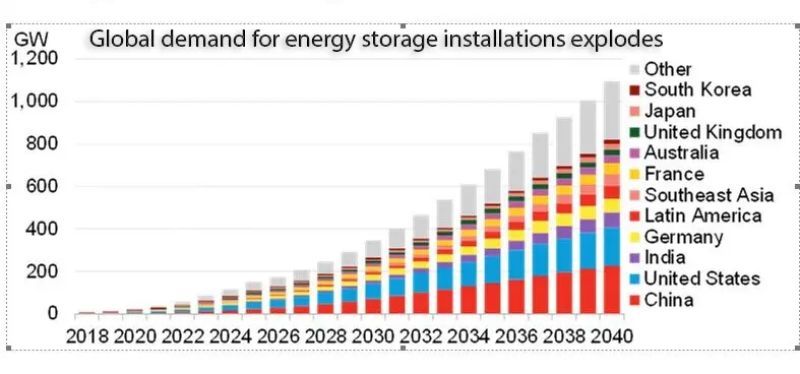

5.The outbreak of global demand continues to drive China's leading companies to accelerate their global layout

Strict carbon emission reduction policies, strong incentives for energy storage investment subsidies, and a more market-oriented power operation market make the global energy storage installed capacity and product gross profit space at this stage larger than the Chinese market. According to market statistics, in 2021, China's new electrochemical energy storage capacity will be 1.87GW/3.49GWh, and the newly installed non-pumped hydro storage capacity will reach 2.09GW.

During the same period, the American Clean Energy Association recently announced that the installed capacity of utility-scale battery energy storage systems deployed in China (excluding the post-meter installed market such as home storage) reached 2.6GW/10.8GWh, 1.5 to 3 times that of China. Australia, South Africa, the European Union and the Middle East also have huge demand waiting to be tapped. The export-oriented feature of China's energy storage market of "production inside and export" will continue in 2022.

Stimulated by global demand, China's top energy storage companies are all gearing up in 2021 to accelerate their global deployment. For example, at the end of 2021, Huawei won the bid for the 1.3GWh Red Sea New City microgrid project in Saudi Arabia, and EVE signed a two-year battery cell supply agreement with Powin, an American system integrator, stipulating that EVE will provide at least 1GWh of LFP power to the other party in the next two years. core. It is predicted that the fire and explosion accident of lithium battery energy storage power stations using ternary cells in the world will be difficult to solve in the short term. In 2022, Chinese LFP energy storage cell and system suppliers will usher in more GWh-level purchase orders. The export of cells and systems will enter the GW era.

6.More central and state-owned enterprises will join the energy storage track in China

Energy storage and renewable energy have natural synergy and complementarity, and are also an indispensable new energy infrastructure in the new power system in the future. Since 2021, central and state-owned enterprises represented by State Grid Corporation of China, China Southern Power Grid, and State Power Investment Corporation have successively formulated their own carbon neutrality routes, and invariably adopted energy storage as a key means to achieve carbon neutrality. For example, State Grid strives to increase the installed capacity of pumped storage power stations in the company's operating area from the current 26.3 million kilowatts to 100 million kilowatts, and electrochemical energy storage from 3 million kilowatts to 100 million kilowatts by 2030. It will reach 7.5GW, and the cumulative installed capacity of energy storage will reach 20GW in 2035.

It is expected that in 2022, more central and state-owned enterprises will propose and implement their 14th Five-Year Energy Storage Development Plan, which will drive the investment and financing scale of the energy storage industry chain to a new level. Central state-owned enterprises are expected to become the main force for energy storage investment and construction in the 14th Five-Year Plan. When it comes to energy storage, home energy storage is also a very important part, and people pay a lot of attention to it. You may be interested in Top5 home energy storage companies in China, if you want to get to know more about the home energy storage companies in China, you can read the Top5 home energy storage companies in China in 2021 in our website. In that article, we introduced Top5 home energy storage companies in detail.