Main content:

- Changes in battery lithium carbonate and lithium hydroxide prices in May

- Supply and demand structure of battery grade lithium carbonate: small cyclic increase

- Supply and demand structure of industrial grade lithium carbonate: both increased significantly

- Lithium hydroxide supply and demand structure: export increment

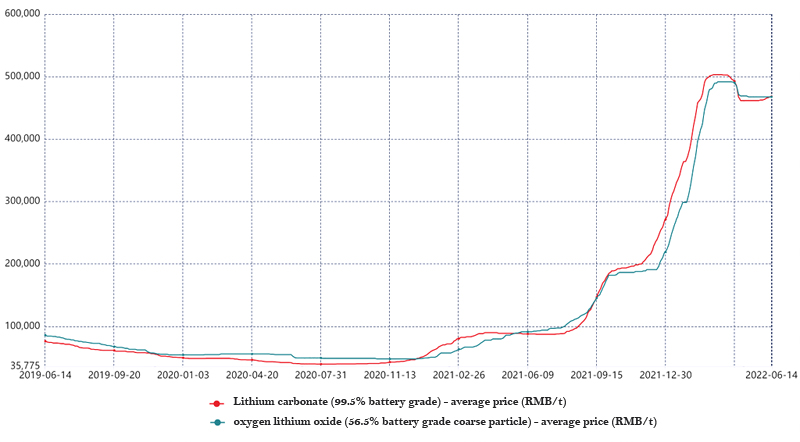

The monthly average price of battery-grade lithium carbonate in May was 461,657 RMB/ton, down 5% from the previous month; the monthly average price of battery-grade lithium hydroxide was 467,815 RMB/ton, down 3% from the previous month. As the price of lithium carbonate falls, the power battery industry chain is also expected to gradually return to rationality. This article will conduct a detailed analysis of the lithium industry prices in May, and predict the trend of June in terms of the current form. Maybe you will want to know about power battery companies, reading the Top 10 power battery companies on our website will help you understand the latest developments of these battery companies.

1.Changes in battery lithium carbonate and lithium hydroxide prices in May

The average price of battery grade lithium carbonate in May was 461,657 RMB/ton, down 5% month-on-month. At the beginning of the month, the supply side due to the release of new capacity gradually up. On the demand side, the production schedule of lithium iron phosphate is expected to turn slightly better, other materials remain low, the overall demand rises slightly, and the price of lithium carbonate is stable. In the middle of the month, the supply side is stable, the upstream attitude is dominated by the offer price, some companies due to inquiries and slightly improved attitude of downstream, overlay ore auction news for the cost side may increase uncertainty in the mood and expectations, the overall offer will be strong.

In terms of downstream companies, as most of the demand for better signals still stay at the expected level, for lithium purchase also tends to be cautious. Prices fell slightly as supply and demand remained tight. At the end of the month, the supply side was stable. Small and medium-sized companies and traders in the previous downward market had a strong strength to sell goods. The inventory was low and the demand showed signs of recovery. The newly added iron lithium capacity has an increase in industrial carbon and quasi-electricity, while some small and medium-sized companies have just need to purchase, and the supply of low-price goods in the market has decreased significantly, and the price has risen rapidly at low amplitude, and the price has risen.

The average monthly price of battery grade lithium hydroxide in May was 467,815 RMB/ton, down 3% from the previous month. June driven by lithium carbonate prices, prices may edge up. Lithium hydroxide prices edged down earlier this month. On the supply side, new capacity is rising steadily. On the demand side, some battery companies still reduce the storage of high nickel three RMB, and some material companies hold more positive expectations for high nickel demand in June, so the market is slightly more active, but the actual transaction is still less. In the middle of the month, the supply side edged up.

On the demand side, due to weak demand and no obvious signal of demand recovery, downstream material companies have weak inquiries and purchase intentions for lithium hydroxide, low market activity, and the price has a slight downward trend. At the end of the month, the supply side increased slightly, but the demand side basically maintained, a small surplus situation is still in. In terms of market performance, the market activity is still low, and the mainstream major companies are not willing to sell at a low price because the market in other countries is still strong. Some small and medium-sized Chinese companies that do not export products have lower prices and stronger transaction intentions. Because most of the downstream material companies are still pessimistic. Overall market stalemate to maintain price stability.

2.Supply and demand structure of battery grade lithium carbonate: small cyclic increase

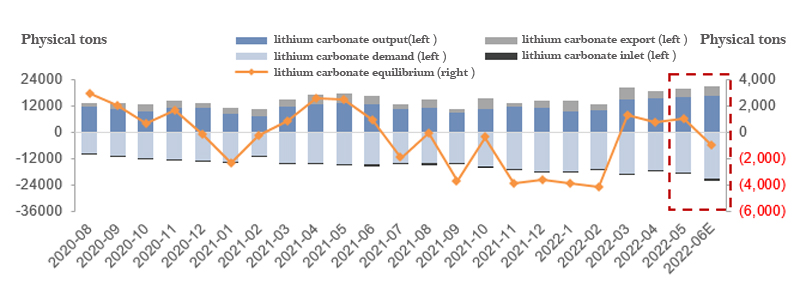

On the supply side, China's battery grade lithium carbonate production in May 2022 was about 15,918 tons, up 1% month-on-month and 19% year-on-year. In May, pyroxene, mica and Salt Lake raw material smelters underwent alternation maintenance, and the overall production remained stable. However, due to the rapid decline of carbon price, the purification part increased slightly. After June, the production capacity of some mica smelters was released, resulting in a small increase in supply.

Meanwhile, driven by the recovery of demand, the output of purification companies increased. China's production of battery grade lithium carbonate is estimated to be about 16,793 tons in June, up 5% month-on-month. On the demand side, China's battery grade lithium carbonate demand increased 5% in May and 27% year-on-year. Ternary materials as cathode materials for ternary lithium battery, may orders run low, medium and low nickel production slightly improved. Lithium cobalt acid still maintain off-season market, overall stable demand. As the epidemic situation improves, the terminal demand and battery start up gradually recover, the demand for iron lithium bottomed out and rebounded, and the demand for lithium carbonate increased by about 10%.

After entering June, lithium cobalt is generally stable, after the epidemic stage power market demand continues to pick up, lithium iron market demand is expected to be positive, production recovery is more radical, part of the new iron lithium plant is about to put into production, at the same time, three aspects also with the recovery of power demand, production has risen, the overall demand for electricity carbon increased significantly. Overall electricity demand is expected to rise 17 percent in June.

In terms of import and export, after May, as the epidemic was under control, part of the lithium carbonate stored in the port gradually entered the Chinese market, and the import volume may be significantly higher than that of April, and the pressure of stock exhaustion has increased in the short term. In June, customs logistics resumed, followed by a steady increase in global lithium carbonate supply, import value may still remain high.

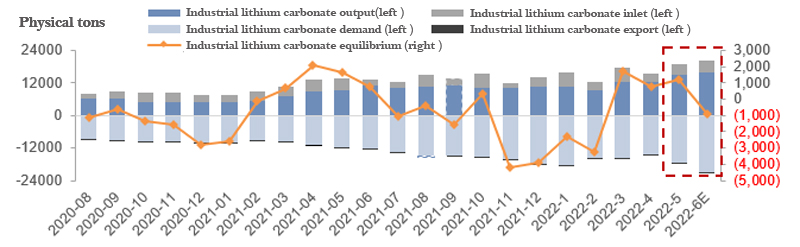

3.Supply and demand structure of industrial grade lithium carbonate: both increased significantly

On the supply side, China's industrial lithium carbonate output in May 2022 was about 14,973 tons, up 20% month-on-month and 57% year-on-year. Production in Qinghai region of China is approaching its peak gradually, and some mica companies have resumed their maintenance and released new production capacity, resulting in a significant increase in supply. In June, the newly added capacity of some companies continued to climb, and the production in Qinghai region reached the peak of production. The overall industrial carbon output still showed a further upward trend compared with May. China's industrial production of lithium carbonate is expected to be about 15,982 tons in June, up 7% month-on-month.

On the demand side, industrial grade lithium carbonate demand rose 22 percent in May. In terms of lithium iron phosphate, the power market demand gradually picked up after the epidemic improved, and with the increase of lithium iron production, the demand for external production increased significantly. In terms of lithium manganate, the downstream demand recovered slightly after the lithium price increased slightly in late May, and then the purchase demand increased slightly compared with April. Enter June, because the terminal demand is expected to be better lithium iron phosphate production radical, is expected to June total industrial carbon demand or up 19%.

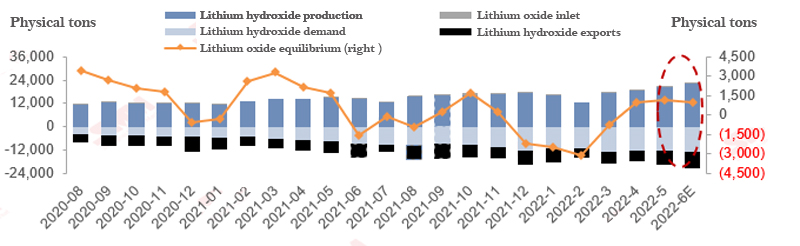

4.Lithium hydroxide supply and demand structure: export increment

After entering June, with part of the head companies repair has been restored, while the new production line continues to climb, the overall lithium hydroxide supply or still a small increase. China is expected to produce 21,922 tons of lithium hydroxide in June, up 6% month-on-month. On the demand side, China's power market gradually recovered in May, but some some Chinese battery companies, including Top 10 energy storage lithium battery companies, maintained storage reduction measures. And China's high-nickel purchase orders remained low. The global demand increased steadily and slightly, with the overall demand increasing by 1%. Enter June, terminal demand recovery, global high nickel demand up slightly, is expected to lithium hydroxide total demand up 7%.

Related article: Top 10 lithium battery companies, Top 10 lithium battery separator companies